Table of Contents

Introduction

How does Medicare affect ongoing worker’s compensation injuries? This pressing question often arises for workers who have sustained injuries on the job and are navigating the complex intersection of Medicare and workers’ compensation benefits. Broadly, Medicare acts as a secondary payer in situations where workers’ compensation should cover job-related injuries or illnesses. Here’s a quick overview:

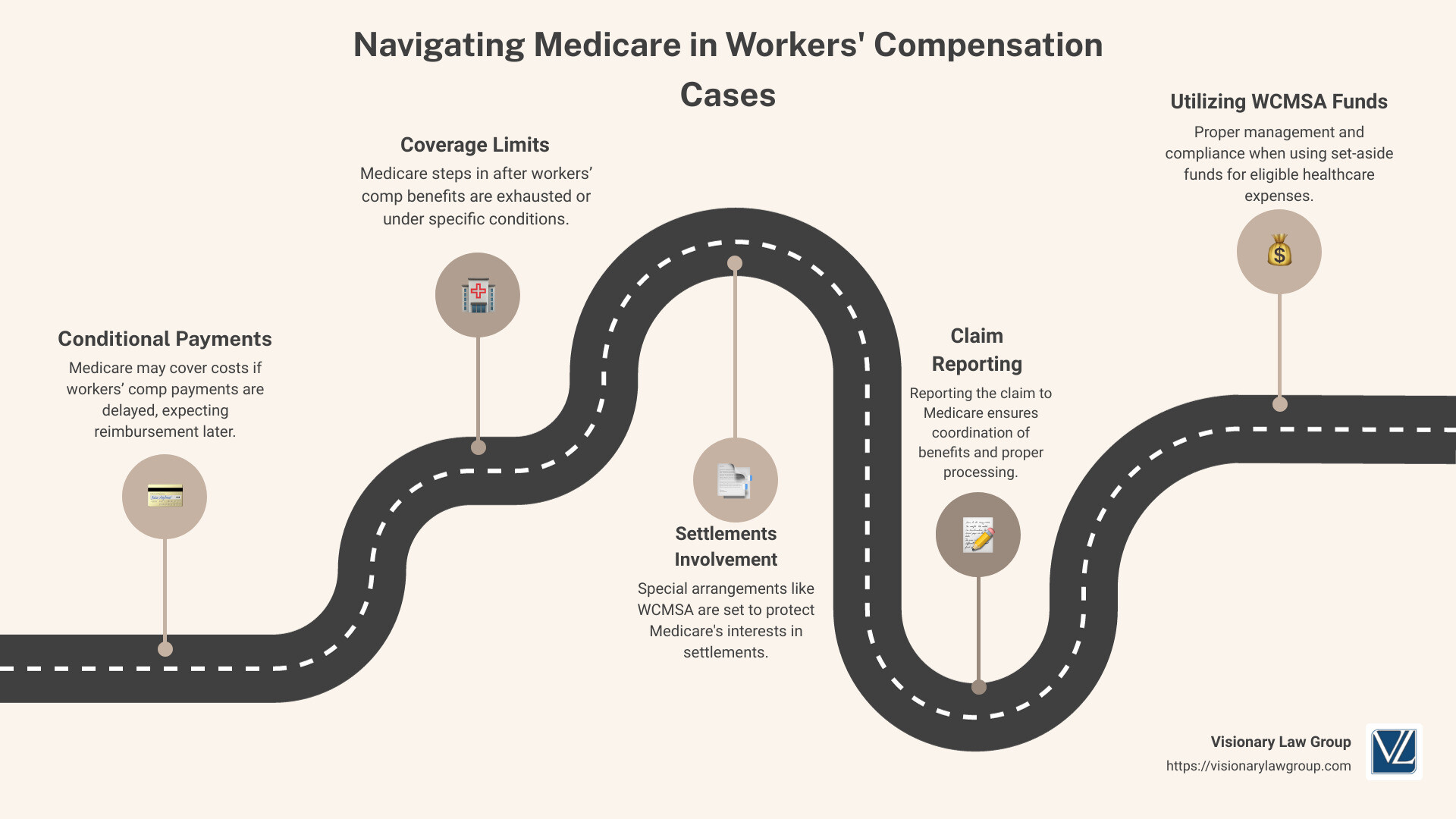

- Conditional Payments: Medicare may make conditional payments if workers’ compensation is delayed, but expects reimbursement.

- Coverage Limits: Workers’ compensation is primarily responsible for job-related medical expenses, yet Medicare can cover related medical costs once worker’s comp benefits exhaust or when specific conditions apply.

- Settlements Involvement: When settling workers’ compensation claims that involve Medicare beneficiaries, special care like a Workers’ Compensation Medicare Set-Aside Arrangement (WCMSA) is necessary to ensure Medicare’s future interests are protected.

Understanding the intertwining of these systems is crucial as it directly impacts your healthcare coverage, out-of-pocket expenses, and overall financial planning during recovery. Navigating this landscape can be daunting; hence, the importance of informative guidance cannot be overstressed.

Understanding Medicare and Workers’ Compensation

When discussing how does Medicare affect ongoing worker’s compensation injuries, grasp the basics of both Medicare and Workers’ Compensation. This understanding will help you navigate the complexities of managing healthcare benefits and claims if you’re injured on the job.

Medicare Basics

Medicare is a federal health insurance program primarily for people aged 65 and older, but it also covers younger individuals with certain disabilities. The program consists of different parts:

– Part A (Hospital Insurance): Covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care.

– Part B (Medical Insurance): Covers certain doctors’ services, outpatient care, medical supplies, and preventive services.

– Part D: Offers prescription drug coverage.

Medicare typically covers 80% of the approved amount for medical services after the deductible has been met, leaving the beneficiary responsible for the remaining 20%.

Workers’ Comp Basics

Workers’ Compensation is a state-mandated insurance program that provides compensation to employees who suffer job-related injuries and illnesses. Unlike Medicare, which is a federal program, Workers’ Compensation laws and benefits vary by state but generally cover:

– Medical expenses related to the injury.

– A portion of the wages the worker loses while they are unable to work.

– Rehabilitation and retraining costs if the worker needs to learn new skills to return to the workforce.

– Compensation for permanent injuries.

Interaction Between Medicare and Workers’ Compensation

When a worker who is eligible for Medicare is injured on the job, the interaction between Medicare and Workers’ Compensation can be complex. Workers’ Compensation is generally considered the primary payer for medical bills related to the workplace injury, meaning it pays before any other health coverage.

However, if there are delays or disputes in the payment of Workers’ Compensation benefits, Medicare may make conditional payments. These are payments that Medicare makes temporarily, with the understanding that they will be reimbursed once the Workers’ Compensation insurer pays.

This coordination ensures that the injured worker receives timely medical treatment without undue financial hardship while the various insurance issues are being resolved. However, it’s crucial for workers to understand that they must notify Medicare of their Workers’ Compensation claim to manage these payments effectively.

Understanding these basics sets the stage for deeper insights into specific scenarios, such as what happens when settling a claim involving Medicare and Workers’ Compensation, which we will explore in the following sections. This knowledge is vital for ensuring that all your medical needs are met without unnecessary out-of-pocket expenses.

How Does Medicare Affect Ongoing Worker’s Compensation Injuries

When you’re dealing with a workplace injury and navigating the complexities of both Medicare and workers’ compensation, understanding how these systems interact is crucial. This section breaks down the key areas where Medicare impacts ongoing workers’ compensation injuries, including conditional payments, coverage limits, and Medicare’s role as a secondary payer.

Conditional Payments and Their Impact

When a workers’ compensation claim is pending, and medical costs need to be covered immediately, Medicare might step in to make conditional payments. This is crucial to prevent any delay in necessary medical treatments. However, these payments are called “conditional” because they are made with the understanding that Medicare will be reimbursed once the workers’ compensation insurer settles the claim.

120-day rule: If workers’ compensation hasn’t responded to a medical bill within 120 days, Medicare may pay the bill temporarily. It’s important for workers to understand that these payments are not a gift — they are an advance, and Medicare expects to be paid back once the workers’ compensation benefits are sorted out.

Conditional vs. non-conditional payments: If workers’ compensation denies a claim for a service that Medicare covers, Medicare pays on a non-conditional basis. This means you won’t have to repay Medicare for these expenses.

Coverage Limits and Exceptions

Pre-existing conditions: Workers’ compensation might not cover all medical expenses if part of your care involves treatment for pre-existing conditions that were exacerbated by workplace injuries. In these situations, Medicare can cover the gap, paying for the care that relates to the pre-existing condition.

Coverage scope: It’s essential to understand the limits of what Medicare and workers’ compensation cover. Workers’ compensation will cover treatment only for injuries that are directly related to your job. Medicare covers a broader scope of health issues, which can help fill in coverage gaps left by workers’ compensation.

Medicare vs. Workers’ comp: Generally, workers’ compensation will pay first for job-related injuries. Medicare serves as a backup payer, covering additional costs that workers’ compensation does not cover, but only after other payer options have been exhausted.

The Role of Medicare as a Secondary Payer

In the realm of workers’ compensation injuries, Medicare typically acts as a secondary payer. This means:

- Secondary insurance: Medicare steps in only after the primary insurance, which in this case is workers’ compensation, has paid its share.

- Claim forwarding: If you have ongoing medical bills due to a work-related injury, these claims should first be submitted to your workers’ compensation insurance. If they deny the claim or it is delayed, you can then forward these bills to Medicare.

- Coordination of benefits: It’s vital to report any workers’ compensation claims to the Medicare coordination of benefits contractor. This helps ensure that all payments are tracked correctly and that Medicare is reimbursed for any conditional payments.

Navigating the intersection of Medicare and workers’ compensation can be tricky, especially when dealing with ongoing injuries. Understanding these key areas helps ensure that you are not caught off-guard by unexpected medical bills and that you take full advantage of the coverage options available to you. Moving forward, we will delve into how to effectively manage and file workers’ compensation claims involving Medicare, ensuring that all legal and procedural requirements are met for a smooth handling of your case.

Navigating Workers’ Compensation Claims with Medicare

The Process of Filing a Workers’ Comp Claim with Medicare

Filing a workers’ compensation claim when you are a Medicare beneficiary requires careful coordination to ensure that all benefits are utilized appropriately without violating any rules. Here’s a straightforward guide:

-

Claim Submission: Immediately after an injury, notify your employer and seek medical attention. Use the forms provided by your employer or download them from your state’s workers’ compensation board website. Document every detail about the injury and the circumstances surrounding it.

-

Documentation: Gather all medical documentation that links your injury directly to your workplace. This includes medical reports, treatment records, and doctor’s notes. Accurate and thorough documentation is crucial for supporting your claim.

-

Reporting to Medicare: Contact the Medicare Coordination of Benefits Contractor at 800-999-1118. Reporting your injury helps Medicare track which costs should be covered by workers’ compensation and which should fall under Medicare, preventing issues with coverage down the line.

How Settlements Work with Medicare Involvement

When it comes to settling a workers’ comp claim involving Medicare, there are additional considerations to ensure Medicare’s interests are protected:

-

WCMSA (Workers’ Compensation Medicare Set-Aside Arrangement): If your settlement includes future medical expenses, setting up a WCMSA is crucial. This fund specifically allocates money for future medical treatments related to your work injury, which must be exhausted before Medicare will begin to cover treatment costs again.

-

Legal Requirements: Ensure that your settlement agreement complies with Medicare requirements. This often involves legal counsel to negotiate terms that consider Medicare’s interests, particularly if your total settlement or future medical expenses are substantial.

-

Future Medical Expenses: Accurately estimating future medical expenses is essential. This amount should be sufficient to cover all expected treatments so that Medicare does not have to pay prematurely. This involves detailed assessments and sometimes consultations with medical professionals.

By understanding these processes, you can navigate the complexities of filing and settling a workers’ compensation claim with Medicare involvement more effectively. This ensures that all your medical needs are addressed and funded appropriately, whether through workers’ compensation or Medicare.

Workers’ Compensation Medicare Set-Aside Arrangements (WCMSA)

Setting Up a WCMSA

Setting up a Workers’ Compensation Medicare Set-Aside Arrangement (WCMSA) is a critical step in ensuring that Medicare’s interests are protected when you settle a workers’ compensation claim that includes future medical expenses. Here’s how to properly establish a WCMSA:

-

Approval Process: Before using the funds, the set-aside amount must be approved by CMS. This involves submitting a detailed proposal that outlines your future medical costs related to the work injury. This proposal is reviewed to ensure that it meets Medicare’s requirements and adequately protects its interests.

-

Fund Management: Once approved, the funds must be placed in a separate account. This account is used solely for medical expenses related to the injury that would otherwise be covered by Medicare.

-

Compliance: It’s crucial to adhere to all rules regarding the use of these funds. Non-compliance can result in Medicare refusing to cover future medical expenses until the misused funds are replenished.

Using Your WCMSA Funds Appropriately

Proper management of your WCMSA funds is essential to ensure that they last until you no longer need treatment for your injury. Here’s what you need to know about using these funds:

-

Eligible Expenses: Only use your WCMSA funds for medical and prescription expenses related to your work injury that Medicare would otherwise cover. This includes doctor visits, medication, and necessary medical equipment.

-

Record Keeping: Keep meticulous records of all expenditures from your WCMSA. Save receipts, bills, and detailed notes about each medical service received. This documentation is crucial in proving to Medicare that the funds were used appropriately.

-

Fund Depletion: After all the set-aside funds have been used correctly for eligible expenses, Medicare will begin to cover eligible medical costs related to the injury. It’s important to notify Medicare once the funds are depleted to ensure a smooth transition.

By understanding and following these guidelines, you can manage your WCMSA effectively, ensuring that your future medical needs are met without jeopardizing your Medicare coverage.

Frequently Asked Questions about Medicare and Workers’ Comp

Does Medicare Have to Be Repaid?

When dealing with how does medicare affect ongoing worker’s compensation injuries, it’s crucial to understand the repayment obligations tied to Medicare. If Medicare makes conditional payments for your work-related injury while awaiting the resolution of your workers’ compensation claim, you are required to repay Medicare. These conditional payments are made only when the workers’ comp doesn’t pay promptly (within 120 days) and are meant to be a temporary solution.

Once your workers’ compensation claim is settled, or a judgment is made, you must reimburse Medicare for the expenses it covered that should have been paid by workers’ comp. This repayment ensures that Medicare can continue to function effectively for all beneficiaries.

Does Medicare Cover On-the-Job Injuries?

Medicare typically acts as a secondary payer in cases where workers’ compensation is involved. This means that workers’ comp is the primary payer for all job-related injuries. However, if workers’ comp denies a claim or fails to make a decision within 120 days, Medicare may step in to make conditional payments. These payments are crucial as they ensure that you receive the necessary medical care without delay.

Medicare will seek reimbursement for these conditional payments once your workers’ compensation claim is resolved. Therefore, while Medicare does cover on-the-job injuries under specific conditions, it does so with the expectation of being repaid once workers’ compensation benefits are received.

How Does Returning to Work Affect Medicare?

Returning to work after an injury can have implications for your Medicare coverage, especially if you receive health insurance through your employer. If you are covered under an employer’s health plan and also eligible for Medicare, your employer’s plan will be the primary payer for any non-work related health care. Medicare will generally serve as the secondary payer.

However, if you return to work and your employer does not offer health insurance, or if you’re not eligible for the employer’s plan, Medicare will continue as your primary health insurance provider. It’s essential to inform both your employer and Medicare about any changes in your employment status or health coverage to ensure that your medical bills are processed correctly.

In summary, understanding the interplay between Medicare and workers’ compensation is crucial for effectively managing your health care needs and financial responsibilities. Whether dealing with repayment obligations, coverage during employment, or conditional payments, being informed helps you navigate the complexities of these two programs.

Conclusion

At Visionary Law Group LLP, we are dedicated to empowering injured workers by providing expert legal representation and clear, understandable guidance. Navigating the complexities of workers’ compensation and Medicare can be daunting, but you don’t have to face it alone. We are here to ensure that you understand your rights and the benefits available to you, helping you take active steps towards recovery and securing the compensation you deserve.

Our experienced attorneys specialize in the intersection of workers’ compensation and Medicare, ensuring that all aspects of your case are handled with precision and care. From managing Workers’ Compensation Medicare Set-Aside Arrangements (WCMSA) to advising on conditional payments and coverage limits, our team is equipped with the knowledge and expertise to maximize your benefits and protect your interests.

We understand that each case is unique, and our approach is tailored to meet your specific needs and circumstances. By partnering with us, you can expect a partnership that values transparency, responsiveness, and a commitment to achieving the best possible outcome for your case.

Don’t let the burden of a workplace injury disrupt your life more than it has to. Take the first step towards a secure and stable future by scheduling a free case evaluation with Visionary Law Group LLP today. Let us help you navigate the path to recovery and ensure that you are fully supported every step of the way. Together, we can secure the compensation and care you rightfully deserve.