Table of Contents

Calculate value permanent total disability claim is an essential process when dealing with disability claims. Understanding this calculation is crucial to ensure that you or your loved ones receive the full benefits deserved after a life-altering injury. Here’s a quick overview of what’s involved:

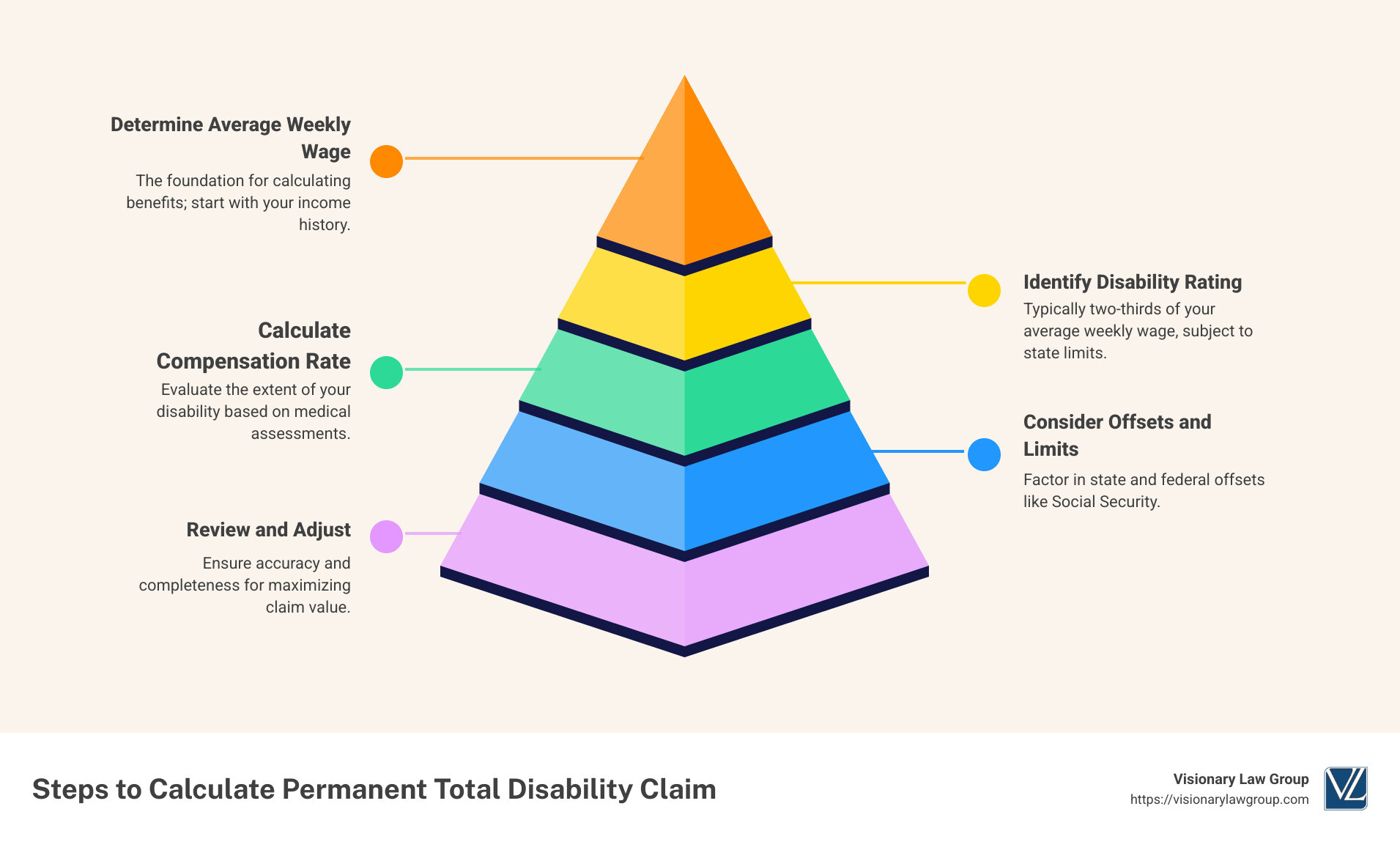

- Determine your average weekly wage, as this forms the basis for calculating benefits.

- Rate of compensation is generally two-thirds of your average weekly wage, subject to state-specific limits.

- Consider state and federal offsets, such as Social Security, that may affect your benefits.

Permanent total disability claims are significant because they often represent a lifetime of financial support for those who can no longer work. This process can be overwhelming, but understanding it will empower you to achieve a fair outcome. By ensuring all aspects of your claim are maximized, you stand a better chance of connecting with the compensation you are rightfully owed.

In my experience as an attorney, having assisted clients through the complexities of calculating the value of permanent total disability claims, I’ve seen the impact of accurate and thorough claim calculation. This expertise allows me to guide clients to successfully navigate their claims.

Understanding Permanent Total Disability

Permanent Total Disability (PTD) is a condition where an individual can no longer engage in any form of gainful employment due to severe injury or illness. This status is more than just a temporary setback; it signifies a permanent change in one’s ability to work and earn a living.

Definition and Qualifications

To qualify for PTD benefits, an individual must demonstrate a complete inability to return to work. This can be due to:

- Total and permanent loss of sight in both eyes

- Loss of both arms at the shoulder

- Loss of both legs near the hips, making prosthetics unusable

- Complete and permanent paralysis

- Total and permanent loss of mental faculties

In addition to these conditions, there are specific criteria for injuries occurring after October 1, 1995. For instance, an individual must have a certain percentage of permanent partial disability (PPD) rating, which varies based on age and educational background.

Total Disability

Total disability implies that the individual cannot perform any job, not just their previous occupation. This is a critical distinction because it broadens the scope of what it means to be “totally disabled.”

- Example: Consider a construction worker who suffers a severe back injury. If they cannot perform any job due to this injury, they may qualify for PTD benefits, ensuring financial stability despite their inability to work.

Importance of Accurate Calculation

Calculating the value of a permanent total disability claim involves understanding your average weekly wage and the specific compensation rate applicable in your state. Typically, this is two-thirds of your average weekly wage, but it is essential to consider any state or federal offsets like Social Security Disability Insurance (SSDI) benefits.

Understanding these elements can make a significant difference in the benefits you receive. By knowing how to accurately calculate your claim, you ensure that you receive the full financial support you deserve.

In the next section, we will dive deeper into the calculation of the value of a permanent total disability claim, exploring the disability rating and formulas involved.

How to Calculate Value of Permanent Total Disability Claim

When dealing with a permanent total disability (PTD), it’s essential to understand how to calculate the value of your claim to ensure you receive the financial support you need. Here, we’ll break down the key components involved in this calculation: disability rating, average weekly wage, and the calculation formula.

Disability Rating

The disability rating is a percentage that indicates the extent of your impairment. This rating is determined through a medical evaluation and plays a crucial role in calculating your PTD benefits. For example, a high impairment rating, such as 40% for severe spinal injuries, can lead to significant compensation. In Texas, each percentage point of impairment contributes to the overall benefits received.

Average Weekly Wage

Your average weekly wage (AWW) forms the basis of your PTD benefits. It’s typically calculated based on your earnings before the injury. For instance, if you earned $900 a week, your PTD benefits would generally be two-thirds of that amount, resulting in $600 per week. This ensures that your financial support reflects your pre-injury earnings.

Calculation Formula

The formula for determining PTD benefits involves several steps:

-

Determine the Average Weekly Wage (AWW): Sum up your earnings over a specific period and divide by the number of weeks.

-

Apply the Compensation Rate: Multiply the AWW by the compensation rate, usually two-thirds, to get the weekly benefit amount.

-

Consider Offsets: If applicable, account for any offsets like Social Security Disability Insurance (SSDI) benefits. For example, in Wisconsin, the state’s reverse offset approach allows for adjustments to ensure total benefits don’t exceed 80% of your average earnings.

Example Calculation

Suppose you have an AWW of $900, a disability rating of 50%, and you’re eligible for SSDI benefits. Here’s how you might calculate your PTD benefits:

- Base Weekly Benefit: $900 (AWW) x 2/3 = $600

- Account for SSDI Offset: If SSDI benefits are $300 per week, your state benefits might reduce to $300 to maintain the 80% cap on total benefits.

By understanding these steps and using available tools like a work injury compensation calculator, you can accurately determine the value of your PTD claim.

In the next section, we’ll explore the various factors affecting your claim, including changes in disability rating, wages, and the impact of the injury date.

Factors Affecting Your Claim

Several factors can influence the value of your permanent total disability (PTD) claim. Understanding these can help you maximize your benefits and ensure you receive the compensation you deserve.

Disability Rating

Your disability rating is a key factor in determining your PTD benefits. This percentage reflects the severity of your impairment and is assessed through a medical evaluation. A higher disability rating typically leads to more weeks of benefits. For example, a 30% disability rating might entitle you to benefits for a significantly longer period than a 10% rating.

Wages

Your average weekly wage (AWW) is the foundation for calculating your benefits. It’s crucial to accurately calculate your AWW by including all earnings, such as overtime and non-pecuniary benefits. A higher AWW results in higher weekly benefits since PTD benefits are generally two-thirds of your AWW. For instance, if your AWW is $900, your weekly benefit might be approximately $600.

Injury Date

The date of your injury can also affect your claim. This is because state laws and benefit rates may change over time. For instance, if you were injured before a legislative change that increased benefit caps, your compensation might be lower than for someone injured after the change. It’s essential to check the specific rules and rates applicable at the time of your injury.

Social Security Offset

If you receive Social Security Disability Insurance (SSDI) benefits, a social security offset may apply. Federal law mandates that total benefits from SSDI and workers’ compensation should not exceed 80% of your average current earnings. In states like Wisconsin, a reverse offset is used, meaning your workers’ compensation benefits are adjusted to comply with this cap. This ensures that your total benefits do not surpass the allowed limit, which might affect the final amount you receive weekly.

Understanding these factors is crucial for accurately calculating the value of your PTD claim. In the next section, we’ll address some frequently asked questions about permanent total disability claims to help you steer this complex process.

Frequently Asked Questions about Permanent Total Disability Claims

Navigating the intricacies of permanent total disability (PTD) claims can be challenging. Here, we address some common questions to help you understand the process better.

How is permanent total disability calculated?

The calculation of PTD benefits is primarily based on your average weekly wage (AWW) at the time of your injury. Typically, PTD benefits are set at two-thirds of your AWW. For instance, if your AWW was $900, your weekly PTD benefit would be approximately $600. This ensures that workers receive a substantial portion of their income to help cover living expenses while they cannot work.

How do I calculate how much disability I will receive?

To determine how much disability compensation you will receive, start with your average weekly earnings before the injury. Calculate two-thirds of this amount to find your weekly benefit. Be aware that there is often a maximum weekly compensation limit set by state law, which caps the amount you can receive regardless of your previous earnings. It’s crucial to check the specific cap applicable in your state to understand the maximum benefits you might receive.

What is the PD rate and how is it determined?

The Permanent Disability (PD) rate is calculated similarly to PTD benefits. It is based on a percentage of your AWW, typically two-thirds, and is determined by your disability rating. This rating reflects the extent of your injury’s impact on your ability to work. For example, a higher disability rating signifies a more severe impairment, potentially leading to a longer duration of benefits. Understanding your PD rate helps in estimating the total value of your claim.

By understanding these key components, you can better anticipate the benefits you might receive and ensure that your claim accurately reflects your situation.

Conclusion

At Visionary Law Group, we understand that navigating the complexities of permanent total disability (PTD) claims can be overwhelming. Our mission is to empower you with the knowledge and support you need to maximize your claim, ensuring you receive the compensation you deserve.

Personalized Legal Representation

We pride ourselves on offering personalized legal representation custom to your unique circumstances. Our team is deeply familiar with California’s workers’ compensation laws and is committed to securing the maximum compensation for you. We know that every case is different, and we take the time to understand your specific needs and objectives, providing clear and understandable advice every step of the way.

Free Case Evaluation

We offer a free case evaluation to help you understand your options and how we can assist you. During this consultation, we’ll discuss the facts of your case, gather necessary medical evidence, and represent you at hearings if needed. Our goal is to increase your chances of approval and make the process as smooth as possible.

Don’t let the complexities of the disability claims process deter you from seeking the benefits you deserve. Empower yourself with the support and expertise you need.

Get a free case evaluation with Visionary Law Group today. Your journey to recovery and financial security starts now.